Storm damage insurance claim processes can be daunting after a devastating storm sweeps through your property, leaving behind a trail of destruction. Whether it’s wind, hail, or water damage, filing an insurance claim can feel like navigating a maze. To help simplify the process and get you on the path to recovery, understanding the essentials is crucial:

- Assess and Document: Carefully assess all damage and document it with photos and videos.

- Secure Your Property: Make necessary emergency repairs to prevent further damage.

- File Quickly: Notify your insurance company promptly with all required documentation.

- Understand Your Coverage: Know what your policy covers and any exclusions that may apply.

In Florida, where storms are frequent and fierce, these steps are even more critical. EC Law Counsel is ready to support you, ensuring your claim is handled swiftly and fairly.

By addressing these key steps, you can manage the storm damage insurance claim process effectively and seek the compensation you deserve. And remember, you’re not alone in this journey—EC Law Counsel is here to guide you through every twist and turn.

Understanding Storm Damage Insurance Claims

When it comes to storm damage insurance claims, knowing what your policy covers can make a world of difference. Let’s break it down so you can steer this process with confidence.

Coverage Basics

Homeowners insurance often covers various types of storm damage, but know the specifics of your policy. Generally, it includes:

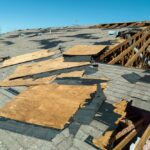

- Wind Damage: This is one of the most common claims. High winds can damage roofs, siding, and windows. Many policies cover these repairs, but in hurricane-prone areas like Florida, you might face higher deductibles.

- Hail Damage: Hail can severely impact your roof and siding. Most insurance policies will cover this, but if you live in a region with frequent hailstorms, a separate windstorm and hail policy might be necessary.

- Water Damage: If a storm causes rain to enter your home through a damaged roof or windows, this is typically covered. However, water damage from flooding is usually not included and requires separate flood insurance.

Exclusions to Watch For

Not all storm-related damages are covered. Here are common exclusions:

- Flood Damage: Standard homeowners policies don’t cover flood damage. Given Florida’s susceptibility to hurricanes and tropical storms, having separate flood insurance is crucial.

- Earthquake Damage: While less common in Florida, it’s worth noting that earthquake damage is not covered under standard policies.

- Wear and Tear: Insurance covers sudden, accidental damage, not gradual wear and tear. If your roof is old and leaks during a storm, your claim might be denied due to poor maintenance.

Understanding these details ensures you’re prepared when a storm hits. EC Law Counsel is here to help you steer these complexities and ensure you receive the compensation you deserve.

In the next section, we’ll dive into the step-by-step process of filing a storm damage insurance claim, so you can take action confidently and efficiently.

How to File a Storm Damage Insurance Claim

Filing a storm damage insurance claim can seem daunting, but breaking it into simple steps can make it manageable. Here’s how you can steer this process smoothly.

Document Damage

Start by documenting all the damage right after the storm. This is crucial for a successful claim.

- Take Photos and Videos: Capture every detail, both inside and outside your home. Include wide shots and close-ups. This visual evidence is essential.

- Make a List: Write down all damaged items and areas. Be thorough and include even minor details like cracked paint or warped floorboards.

Emergency Repairs

Prevent further damage by making temporary repairs. This is not just smart; it’s often required by your policy.

- Cover Holes: Use tarps to cover any roof damage. This helps prevent water from causing more harm.

- Secure Windows: Board up broken windows to keep out rain and debris.

Remember to keep receipts for any materials you buy for these emergency fixes. Your insurer may reimburse you.

Contact Your Insurer

Notify your insurance company about the damage as soon as possible. Here’s how to do it:

- Call or Use an App: Most insurers allow claims to be filed online or via an app. Quick action can speed up the process.

- Provide Details: Have your policy number and the list of damages ready. This will help your insurer process the claim efficiently.

In Florida, where storms are frequent, it’s especially crucial to act fast to get ahead in the queue of claims.

Policy Review

Understanding your policy can prevent surprises later on.

- Check Coverage: Know what your policy includes and excludes. For instance, flood damage typically requires separate insurance.

- Understand Your Deductible: Be aware of the amount you’ll need to pay out-of-pocket before your insurance kicks in. In hurricane-prone areas, this might be higher.

Reviewing these details ensures you’re fully prepared for the next steps.

By following these steps, you can file your storm damage insurance claim with confidence and efficiency. In the next section, we’ll guide you through navigating the claims process, including working with an insurance adjuster and getting repair estimates.

Navigating the Claims Process

Once you’ve filed your storm damage insurance claim, it’s time to steer the claims process. This involves working with an insurance adjuster, obtaining repair estimates, maintaining communication records, and reviewing the settlement offer.

Working with the Insurance Adjuster

After reporting the storm damage, your insurance company will send an adjuster to assess the damage. This is a critical step in the claims process.

- Be Present: Make sure you’re available when the adjuster visits. This allows you to point out all the damage and provide any documentation you’ve gathered.

- Provide Documentation: Show the adjuster your photos, videos, and detailed list of damages. This helps ensure nothing is overlooked.

- Ask Questions: Don’t hesitate to ask about anything you don’t understand. This is your chance to clarify how the claim will be processed.

Obtaining Repair Estimates

Getting multiple repair estimates is essential to ensure fair compensation.

- Contact Reputable Contractors: Reach out to several contractors for quotes. This helps you understand the market rate for repairs.

- Compare Estimates: Look at each estimate closely. Consider the scope of work and the materials used, not just the price.

- Submit to Insurer: Once you have your estimates, submit them to your insurance company as part of your claim. This supports your request for a fair settlement.

Maintaining Communication Records

Keeping detailed records of all communications with your insurer is vital.

- Document Conversations: Note down dates, names, and details of every conversation you have with your insurance company and adjuster.

- Save Correspondence: Keep copies of all emails, letters, and official documents related to your claim.

This organized approach can help resolve any disputes or misunderstandings that may arise.

Reviewing the Settlement Offer

After the adjuster submits their report, your insurer will provide a settlement offer.

- Understand the Offer: Review it carefully to ensure it covers all the damage and matches your policy’s terms.

- Negotiate if Necessary: If the offer is lower than expected, don’t be afraid to negotiate. Provide evidence from your documentation and repair estimates to support your case.

By staying organized and proactive, you can steer the claims process more effectively. This increases your chances of receiving a fair settlement and getting your home back to its pre-storm condition.

In the next section, we’ll explore common challenges you might face during this process and how to overcome them.

Common Challenges and Solutions

Filing a storm damage insurance claim can be tricky. Let’s look at some common challenges and how to handle them.

Deductibles

A deductible is what you pay out of pocket before your insurance kicks in. It can vary based on your policy.

- Understand Your Deductible: Know the amount before filing a claim. For example, if your deductible is $1,000 and the damage is $2,000, you’ll only get $1,000 from your insurer.

- Budget for Deductibles: Keep this amount in savings. If you live in a storm-prone area like Florida, it’s crucial to be prepared.

Policy Limits

Policy limits are the maximum amount your insurer will pay for a covered loss.

- Know Your Limits: Check your policy to see how much coverage you have. This helps set realistic expectations for your claim.

- Adjust Coverage if Needed: If your limits are too low, consider increasing them before the next storm season.

Exclusions

Exclusions are specific situations or types of damage not covered by your policy.

- Read the Fine Print: Understand what your policy excludes. Common exclusions include flood and earthquake damage.

- Buy Additional Coverage: If you need protection from excluded events, like floods, purchase separate policies.

Strategic Filing

Filing strategically can maximize your claim and minimize stress.

- Document Everything: Take photos, videos, and notes of all damages. This evidence is key for a successful claim.

- File Promptly: Report damage to your insurer as soon as possible. Quick filing can lead to quicker payouts.

- Seek Professional Help: Consider consulting with a public adjuster or attorney if you’re unsure about the process. They can guide you through complex claims.

By understanding these challenges and planning ahead, you can make the insurance claim process smoother.

In the next section, we’ll answer some frequently asked questions about storm damage insurance claims.

Frequently Asked Questions about Storm Damage Insurance Claims

What does insurance cover in a storm?

Homeowners insurance typically covers a variety of storm-related damages. Here’s a quick overview:

- Wind Damage: This is commonly covered and includes harm to roofs, siding, and windows. If wind-driven rain enters through a damaged roof or window, that’s usually covered too.- Hail Damage: Hail can severely damage roofs and siding, and most policies will cover repairs or replacements.- Water Damage: Water that enters your home due to a storm, like through a broken window or damaged roof, is generally covered. However, it’s crucial to note that this doesn’t include flooding.

What is not covered by homeowners insurance?While your policy covers many storm-related issues, there are notable exclusions:

- Flood Damage: Flooding is not covered under standard homeowners insurance. If you live in a flood-prone area, consider purchasing separate flood insurance.

- Earthquake Damage: Earthquakes are another exclusion. You’d need a separate earthquake insurance policy if you’re in a high-risk area.

- Wear and Tear: Insurance doesn’t cover damages due to normal wear and tear or lack of maintenance. For example, if your old roof leaks during a storm, it might not be covered.

How long does it take to get a payout from homeowner’s insurance?

The timeline for receiving a payout can vary, but here’s a general idea:

- Claim Timeline: It can take anywhere from a few weeks to several months, depending on the claim’s complexity and the efficiency of your

Eunice Cabrera

Attorney Eunice Cabrera has a unique advantage when it comes to property damage claims. Because she has worked extensively on both ends as an adjuster and as a litigator, Eunice knows how to properly evaluate a claim and obtain a settlement. She understands the strategies that work to get her clients what they rightfully deserve.